Top Legal Issues Facing the Automotive Industry in 2020

Foley’s Automotive Industry Team has prepared this report examining what the legal landscape is likely to look like in 2020 and beyond. Inside, you will learn about:

Contents

- The Impact of Emerging Technologies on Global Automotive Supply Chains

- 2020 Antitrust Outlook – Antitrust Agency Divergence, The Standards Debate and State Activism Present Enforcement Uncertainty

- Key Employment Issues Facing Employers in the Automotive Industry

- Recent Government Announcements Confirm Importance of International Regulatory Compliance for Automotive Companies

- What We Know Now – Lessons from 2019 to Better Manage Data Privacy in 2020

- The USMCA, With the December 2019 Updates, Will Soon Take Effect. Here’s What to Expect

- NHTSA and Motor Vehicle Safety

- Trends in Leveraging Automotive Patent Portfolios

- 2020 Outlook for Automotive M&A: Will the Good Times Keep Rolling?

- The Unsecured Creditors’ Committee: An Important Protection for Suppliers to Bankrupt Customers

Click here to download the PDF.

We hope you find this report useful and informative. If you have any questions regarding its content or how these considerations may affect your business, please contact your Foley attorney or any of the contributors listed.

The Impact of Emerging Technologies on Global Automotive Supply Chains

By Mark Aiello, Partner and Vanessa Miller, Partner

The intense focus on autonomous vehicles and electrification we see today shows no signs of slowing down: in the new automotive industry, every company is a tech company. As these technologies start to move along the supply chain, automotive companies need to address several important issues:

- Risk-Shifting for Warranty Issues

- Intellectual Property

- Cybersecurity and Data Privacy

- Tariffs and Global Commodities Impacting Sourcing

1. Protecting Your Supply Chain

As we begin the shift from human drivers to some level of autonomous driving, managing warranty risks associated with electrical system components and software will be key. What follows are some steps automotive suppliers can take to mitigate this risk:

- Warranty risk management must be addressed at the contracting phase. OEM purchase orders, as well as their corresponding terms and conditions, contain highly favorable terms for OEM. Traditionally, then, making exceptions and limitations to supplier warranties has been difficult to negotiate. Yet with integration, new technology, and joint development, suppliers can now appropriately allocate risk according to responsibility. Specifications for components or systems should be clearly set forth in contract documents, and efforts should be made to limit or disclaim any inapplicable warranties, including warranties outside the scope of design or integration responsibility.

- Parties must clearly document responsibilities for testing and validation. Automotive suppliers should document their responsibilities for testing electrical system components, systems, and networks, while also clarifying the limits of their responsibility for such testing – at the component, system, and vehicle level.

- Address warranty issues promptly. If a warranty issue arises, it is important for the supplier to quickly identify the root cause(s), implement containment procedures, and establish clean points. In addition, protocols should be established for handling warranty claims and analyzing the root causes of dealer repair codes that could implicate the product.

2. Licensing Strategies to Lower IP Costs

With a car’s new technology and/or smart features, licensing presents an opportunity for OEMs to lower costs by saving on intellectual property development and enforcement. Licensing also poses certain legal risks. When negotiating a licensing agreement, you should carefully consider exclusivity of any licensed feature, ownership of any custom modifications to the licensed feature, and ownership of the data derived from the driver’s use of a vehicle with such a feature. A supplier should also use strong confidentiality and ownership protections for the technology assets, and specifically address rights for any unique specifications to the licensed technology. As new technologies predominate the industry, the structure of your licensing agreement – and the clauses protecting your intellectual property – will become increasingly important.

3. Cybersecurity / Data Privacy

The global automotive cybersecurity market is expected to grow at an unprecedented rate, from $1.34 billion in 2018 to $5.77 billion by 2025.1 Responding to a recent survey from Synopsys and the Society of Automotive Engineers (SAE) International, manufacturers say that it is “likely” or “very likely” that malicious attacks on their software or components will occur within the next 12 months.2

Smart technology also increases the amount of personal information collected by the car, making strong data protection paramount. Doing so entails robust policies in connection with the design goals and use of the products. These policies or standards should consider, among other things, industry best practices, such as those published by SAE.3

Breach of applicable agreements, documentation of root cause(s) and documentary evidence supporting the damages are critical should litigation arise.

4. Navigating Tariffs and Volatile Commodities Markets

In addition to the above considerations, automotive companies need to employ a strategy to navigate fluctuating commodities markets, tariffs and other government regulations involving new technologies.

This means analyzing their existing contracts against the backdrop of the contracts’ dynamics, looking both upstream and downstream in their supply chain. For example, leverage and bargaining power will vary depending upon whether the company is a buyer or seller, where the company falls in the tiered supply chain (OEM—Tier 1— Tier 2), whether the component is specially manufactured, or whether the contract is a single-source requirements contract. The quantities at hand will further affect such companies’ leverage and bargaining power. This is true not just for the product being impacted by tariffs or government regulations, but also for the program order in years past, as well as other products with the same customer/supplier.

According to the Electronic Components Industry Association4: “In today’s digital world, nearly every industry utilizes electronic components and the supply chain for such components is globally interconnected and complex. As a result, the imposition of tariffs on the electronic components will have global consequences for businesses and consumers alike, adding friction and costs to the supply chain that can hinder economic growth for all involved.” An additional cause of bottlenecks in many automotive manufacturers’ supply chains is the worldwide shortage of semiconductors. Increases in demand, coupled with capacity limitations and tariffs, are thus creating shortages of key electronic components for automotive assemblies.

Faced with mostly fixed-price, sole-source requirements contracts for specially manufactured goods, automotive manufacturers have employed different strategies in an attempt to gain leverage and force backwards-looking pricing negotiations. Unfortunately, legal arguments that attempt to rely on these contracts’ force majeure provisions or the doctrine of commercial impracticability have

proven unsuccessful.

Looking forward, automotive companies have a number of avenues they can pursue to shift tariff risk. For example, parties to a supply contract may specifically assign the tariff risk to the seller, by listing the price as inclusive of all “taxes, imports, duties, and tariffs.” Alternatively, the parties to a supply contract may simply require the buyer to pay any tariffs. Other supply chain contracts may include a more open-ended pricing provision, which requires the parties to engage in good faith negotiations regarding price increases if tariffs are imposed.

More complex and longer-term strategies employed by automotive companies include indexing and hedging strategies, or considering whether a machining function can be performed by a third party (or at a facility that is not impacted by the tariffs). These, of course, are strategies that need to be analyzed by a cross-functional team at the company.

2020 Antitrust Outlook – Antitrust Agency Divergence, the Standards Debate and State Activism Present Enforcement Uncertainty

By Greg Neppl, Partner

The antitrust outlook in the United States is marked by uncertainty. This article identifies some issues to watch.

Trump Administration Surprises

Historically, U.S. antitrust enforcement has been marked more by continuity than by abrupt change. During the past few decades, we saw an evolution away from blanket rules of per se legality or illegality under federal law (e.g., resale price maintenance and inflexible merger standards), a greater emphasis on economic analysis of likely competitive effects, and an attempt to strike a balance between overly aggressive enforcement (which inhibits potentially procompetitive conduct benefiting consumer welfare) and overly lenient enforcement (which risks adverse consumer welfare consequences).

We are now three years into the Trump administration, however, and we have seen some surprising DOJ (Antitrust Division) enforcement priorities, efforts and outcomes. We have also seen some surprising agency divergence on both standard essential patent issues and (potentially) the standards for merger reviews. Finally, we have seen unusual activism by state attorneys general and a willingness by DOJ to arbitrate the primary issue (market definition) in most merger reviews. Below we discuss some implications of these surprises.

1. DOJ Challenged Time Warner/AT&T

The first major merger review for Makan Delrahim to consider as DOJ Assistant Attorney General for Antitrust was that of Time Warner/AT&T. DOJ sued to block this vertical deal in November 2017, at least in part based on Delrahim’s view that behavioral relief, historically accepted by DOJ (and FTC) to address vertical merger concerns, should be highly disfavored. Following a bench trial on the antitrust merits, Judge Richard Leon denied DOJ’s injunction request. The D.C. Circuit affirmed Judge Leon’s decision in February 2019.

This litigation outcome is relevant to the prospects for vertical merger challenges by DOJ and FTC in the future. In a related event, on January 10, 2020, DOJ and FTC released for public comment draft Vertical Merger Guidelines, describing the “principal analytical techniques, practices and enforcement policy” of the agencies with regard to vertical mergers. These guidelines, once adopted, will replace DOJ’s Non-Horizontal Merger Guidelines from 1984. The draft Vertical Merger Guidelines largely reflect current agency thinking and practice, and therefore are not very surprising. The draft Vertical Merger Guidelines do not, however, address the agencies’ approach to remedies (including behavioral relief) in vertical mergers, an important issue for businesses and antitrust practitioners.

2. DOJ and FTC Diverge on the Licensing of Standard Essential Patents

DOJ has publicly criticized its sister antitrust enforcement agency — the FTC — in the FTC’s successful district court challenge of Qualcomm’s licensing practices relating to standard essential patents addressing 4G transmission technologies. Such a public disagreement between FTC and DOJ on an antitrust policy question is very unusual. Qualcomm has appealed the May 2019 decision of the U.S. District Court for the Northern District of California to the Ninth Circuit.

While DOJ filed a “Statement of Interest” with the Ninth Circuit in July 2019, arguing that the district court decision “threatens competition, innovation, and national security,” critics of Qualcomm’s licensing practices include trade groups representing the U.S. units of various automobile manufacturers such as BMW, Ford, GM and Toyota, as well as Continental, Denso and Intel.

This Ninth Circuit appeal raises an important policy question regarding the antitrust treatment of certain IP licensing practices, with important implications for automotive industry participants.

3. Potential Agency Divergence on Merger Review Standards

Criticism of antitrust enforcement efforts undertaken by federal antitrust agencies – the FTC and DOJ (Antitrust Division) – is nothing new. Reasonable minds can differ as to whether a particular merger or conduct challenge by the agencies advances the established goal of U.S. antitrust enforcement: to protect competition for the benefit of consumers.

At the same time, however, there is a broader debate over the scope of that established goal and whether the objectives of antitrust enforcement should change and the tools of enforcement should be expanded. While this debate is not new either, it often seems to accelerate in advance of elections, as presidential (and congressional) candidates sometimes embrace antitrust enforcement “reform” as a campaign issue. As antitrust enforcement policy can dovetail with broader political themes – including populism, “big business” power, wealth inequality, labor protections, national security, and data privacy – this should come as no surprise.

The most recent and aggressive “reform” proposals have been advocated by presidential candidates Elizabeth Warren and Bernie Sanders. For example, in 2017, Sens. Warren and Chuck Schumer (and others) rolled out their “Better Deal” platform for the 2018 congressional elections. Sen. Sanders more recently proposed antitrust enforcement reforms that eclipse that “Better Deal” platform. Both propose, among other things, to replace the consumer welfare standard for merger reviews with a broader standard that considers various merger impacts unhinged to “competition” or “competitive effects,” a change that could substantially alter the predictability of merger enforcement by introducing a potentially broad range of policy considerations.

AAG Delrahim has rejected the use of antitrust law to address political and social goals advocated by what is called the “hipster antitrust” movement, while acknowledging that “consumer welfare” includes non-price considerations such as innovation and quality. Meanwhile, FTC Chairman Joe Simons said recently that the FTC is taking “a fresh look” at the consumer welfare standard. The extent to which Delrahim and Simons may diverge on this issue is unclear, but certainly worth watching in 2020. If an advocate of replacing the consumer welfare standard is elected president in 2020, the potential impact on merger reviews would be even more significant.

4. State Attorney General Activism

DOJ (and various state AGs) reached a settlement in the proposed Sprint/T-Mobile merger in July 2019, with the Tunney Act review of DOJ’s Proposed Final Judgment pending before D.C. District Court Judge Timothy Kelly. FCC Chairman Ajit Pai had previously announced his support for the combination (subject to conditions) in May 2019. Nevertheless, other state AGs (led by NY and CA) are challenging the transaction in the Southern District of New York. A trial of the state AG matter concluded on December 20, 2019.

Antitrust opposition by state AGs – at least in the form of an independent legal challenge in court – to a merger approved at the federal level by DOJ or FTC is unusual. This state AG challenge raises at least the possibility of one federal court approving a DOJ Proposed Final Judgment as consistent with the “public interest” standard under the Tunney Act, while another federal court enjoins the transaction (perhaps on antitrust grounds not even asserted by DOJ). At the very least, the parallel state AG challenge here may increase the probability in future transactions that one or more state AGs – not satisfied with a DOJ or FTC settlement agreement – will seek independently to enjoin the transaction, thus exposing transactions to greater timing and deal risk. Merger reviews in the EU, in contrast, are conducted either by the EC (DG COMP) or EU member states, but not at both levels simultaneously.

5. DOJ’s Willingness to Arbitrate Market Definition

In September 2019, DOJ sued to block the proposed acquisition of Aleris Corp. by Novelis Inc., two producers of aluminum for automobile manufacturing. Surprisingly, for the first time, DOJ agreed with the parties to use binding arbitration to define the relevant product market. Whether DOJ (or FTC) will arbitrate this key antitrust issue in other merger challenges is unknown, although, as AAG Delrahim has noted, arbitration could well allow (at least some) merger challenges to be resolved more “efficiently and effectively.”

6. DOJ’s Auto Parts Investigation and Antitrust Compliance Programs

Lastly, we should not forget the lessons of DOJ’s long-running investigation of auto parts suppliers, the largest criminal investigation ever pursued by DOJ’s Antitrust Division, which resulted in charges against some 48 companies and yielded almost $3 billion in criminal fines. Settlements of class action and other private plaintiff claims have reportedly exceeded $1 billion.

An effective antitrust compliance program, in addition to detecting and deterring cartel conduct, now brings additional benefits. While DOJ has historically not given credit for antitrust compliance programs in making charging decisions and sentencing recommendations, it announced changes to both policies in July 2019. These long-needed changes increase the legal benefits of implementing an effective antitrust compliance program.

Key Employment Issues Facing Employers in the Automotive Industry

By Jeff Kopp, Partner and Felicia O’Connor, Associate

As we begin a new decade, automotive companies continue to face complicated employment law issues. These include the changing landscape of marijuana laws and their impact on employment, the implications of new minimum wage laws, and finally, National Labor Relations Board (NLRB) changes that affect both unionized and non-unionized employers. Anticipating changes and embracing proactive leadership will help employers minimize risks of becoming caught up in time-consuming and expensive litigation.

1. Marijuana in the Workplace – A Changing and Complicated Legal Landscape

Simply put, legislation legalizing recreational marijuana is everywhere – and more and more states are heading in that direction. In the automotive industry, where many jobs involve operating heavy equipment and manufacturing safety-related products, drug use in the workplace is a serious concern for employers. The legal landscape of marijuana use is complicated and frequently changing. Although marijuana has become legal for medical purposes and/or recreational use in many states, it remains a Schedule 1 substance under the federal Controlled Substances Act.5 Such substances, at least from the federal perspective, have no currently accepted medical use, and a high potential for abuse. The conflict between state and federal law with respect to marijuana leads to a host of legal and practical implications for employers as marijuana use becomes more common in states that have legalized it in some form.

The first and most important complicating factor for multi¬state automotive employers is that state laws differ and are changing frequently. Many states permit marijuana usage for medical purposes.6 More recently, several states, including Michigan, have legalized marijuana for recreational use as well as medical use. However, guidelines for how employers must deal with these laws are less clear.

A few states, such as Connecticut, have medical marijuana laws that include an anti-retaliation provision, which prohibits employers from terminating an employee for their status as a medical marijuana cardholder or for using marijuana in compliance with the state law.7 Each year, more states are added to the list that permit marijuana use in some capacity and each state law is unique. Employers must determine the parameters of marijuana-related laws in the states in which they operate. Disconnects exist between what medical marijuana patients and recreational marijuana users believe regarding their rights and the actual scope of employees’ rights with respect to marijuana use inside and outside of the work environment.

Additionally, employers must understand the intersection between the Americans with Disabilities Act (ADA) and medical marijuana usage. While employers are never required to permit on-the-job marijuana usage, they are required to reasonably accommodate an employee’s qualifying disability under the ADA and must still engage an employee in the usual interactive process under the ADA. When adverse employment decisions appear too closely related to the disability itself, rather than marijuana usage, courts have reacted negatively.8 In addition, mainstream attitudes toward marijuana usage are changing. Moral opposition to marijuana use will not be a good defense for an employer if a disabled individual seeks relief from legally using marijuana under state law.

A complicating factor that overlays the issue of marijuana usage in the workplace is the lack of any scientifically proven real-time test for impairment. There are a myriad of methods for testing marijuana usage but the most commonly used methods, urinalysis and blood testing, do not indicate whether the testing subject is impaired at the time of the test. New technology for breath testing claims to be able to show impairment but has a much shorter window of time by which the test must be taken and has yet to be proven reliable in detecting impairment.9 As a result, a positive drug test does not necessarily demonstrate than an employee is impaired at work or has used marijuana while working.

Additional considerations include the new laws’ intersection with the Drug Free Workplace Act, as well as the practicality of a zero-tolerance policy for off-duty marijuana use in a tight labor market where employees and applicants are more and more likely to engage in some level of marijuana usage.

In this complicated and changing environment, employers should ensure that their policies regarding drug testing comply with the laws of the states in which they operate, are clear and enforced consistently. Additional consideration is obviously needed for unionized facilities, including looking closely at applicable collective bargaining agreements, and understanding that labor arbitrators often view off-duty conduct differently than workplace misconduct. In states that require accommodation, if an employer wishes to maintain a zero-tolerance drug free workplace policy, it should consider identifying and developing a legally defensible business justification for why it is unreasonable to accommodate off-duty marijuana use. This will require the employer study the science of medical marijuana usage. If no such legally defensible business justification exists for the business, the employer may consider modifying its policy.

The bottom line is that employers should focus on workplace conduct – because they can always deal with specific instances of job impairment related to an employee’s drug or alcohol use. Safety and productivity should remain the overarching goals to dictate decisions regarding employee marijuana and drug use.

2. Implications of Increases in Minimum Wage

Minimum wage changes are also on the horizon. On March 29, 2020, Michigan’s minimum wage will increase from $9.25 to $9.45 per hour.10 In that state, and others subject to an increase in minimum wage, the implications reach beyond pure compliance with the law. It goes without saying that employers should research possible minimum wage increases in the states where they operate (if they pay employees at the current minimum wage) in order to stay compliant with the law. However, these wage increases have implications for employers in the automotive industry, even if the increase does not directly impact their workforce.

Retention and hiring of workers in an already tight labor market may prove increasingly difficult given that the gap between minimum wage and the wages paid to automotive industry production workers is shrinking in some places. Employees, who can get nearly the same wages for less physically demanding work, or positions with more attractive schedules, may choose to leave the demands of the automotive industry for other employment options. As a result, employers should analyze their competition for labor and determine whether any minimum wage increase may make retention and recruiting more difficult.

The challenge is that automotive employers need to retain employees to decrease the burden on hiring and training, and to improve productivity in the plant setting. While we can only do so much to increase starting wages, automotive employers must do all they can to make work in a plant setting as attractive as possible. This means that employers should look at their health and welfare benefits programs and highlight to employees, temporary workers, and potential candidates what those benefits are. Focusing on the on-boarding process and developing a team approach to selection and retention of the best workers is also a sound approach. There is no magic formula here, but employers that are more successful seem to foster a sense of belonging and commitment that results in a more cohesive employee team.

3. Changes to NLRB Standards and Priorities

Finally, this year has seen many changes in the governmental oversight of union workplaces that have continuing implications for all employers. Changes to NLRB standards and priorities will continue to affect unionized and non-unionized employers through 2020. On December 23, 2019, the Board issued a new opinion that lowers the bar for deferring cases to the grievance procedure, returning the standard to one that was in effect prior to an Obama-era opinion that made the deferral standard more onerous for employers. As a result, it is now easier for employers to request that an NLRB charge that is related to a grievance be stayed during the course of the grievance procedure. In addition, the Board will be more likely to defer to the outcome of the grievance procedure rather than engaging in its own investigation and determination of the merits of the charge and the change will apply retroactively to any charges currently pending. This is a good development for automotive employers because they can more easily defend employee claims in the private arbitration context rather than before a more public governmental agency.

Also, in August 2019, the NLRB provided guidance regarding employers’ ability to require employees to sign arbitration agreements in the context of a class action lawsuit. The NLRB concluded that (1) employers can require employees to sign modified arbitration agreements in response to employees opting into a collective action under the Fair Labor Standards Act (FLSA) or corresponding state wage laws; and (2) employers can require that the employees sign the modified agreement or face termination. However, the NLRB emphasized that employers are still not permitted to take adverse action against employees purely for participating in a class action.

Both changes continue the NLRB’s trend of opinions that tend to strengthen employer’s rights and undo union-friendly changes that took place during the Obama era.

Summary

Automotive employers will continue to face an evolving legislative landscape in 2020 that will impact workforces. Employee lawsuits, governmental charges and labor grievances are not going away any time soon. Employers will still must deal with regulatory issues to make sure their operations comply with federal and state laws, all with the backdrop of more liberal drug laws permitting recreational drug use.

At the same time, wages are increasing and retaining the best and brightest will remain challenging unless wage rates are competitive, and employees understand and appreciate the value of their contributions. And while the NLRB and other governmental agencies may be recognizing more employer-friendly enforcement protocols, enforcement agencies like the NLRB, the EEOC, the U.S. Department of Labor, and state agencies are still very active in enforcing the statutes with which they are charged.

The examples in this paper highlight just some of the challenges facing employers in the automotive industry in 2020, where vastly differing state laws, frequently changing standards, and a heightened awareness of employment related issues make practicing employment law anything but routine. Be sure to analyze decisions and policies and involve legal counsel and human resources professionals as you navigate the rugged terrain this decade.

Recent Government Announcements Confirm Importance of International Regulatory Compliance for Automotive Companies

By Greg Husisian | Chair, International Trade & National Security Practice, Partner and Jenlain Scott, Associate

Over the last three years, the current administration has imposed the largest export controls penalty, the second-largest economic sanctions penalty, and four of the ten largest anti-bribery penalties – of all time – signaling that compliance with U.S. international regulations has never been more important.

Automotive companies that source, operate, or sell abroad, for instance, face significant regulatory risk. Doing business in the Middle East, Africa, Latin America, and Asia present issues under the Foreign Corrupt Practices Act (FCPA) (frequent bribery requests), economic sanctions from the Office of Foreign Assets Control (OFAC) (limitations on dealings with Iran, Syria, Russia, Venezuela, and other sanctioned countries), and export controls (restrictions on shipments of U.S.- origin goods to embargoed or restricted countries or persons). Iran presents its own unique concerns as the U.S. government maintains sectoral sanctions that specifically restrict the ability of U.S. companies to deal with the Iranian automotive sector.

This landscape makes it essential that global automotive companies take steps to identify, manage, and minimize their international regulatory risk. Recent guidance from the U.S. government underscores that any such risk analysis must extend to automotive supply chains as well.

While automotive companies have traditionally focused on sales-side issues to evaluate international regulatory risk – assuming that these areas left them most vulnerable – the U.S. government has recently sent several messages detailing an expectation that companies subject their entire supply chain to extensive due diligence, based on state-of-the-art compliance measures. These messages include the issuance of an unusual briefing by the Departments of State, Treasury, and Homeland Security on the need for supply chain due diligence, as well as a special advisory from the Department of Homeland Security on supply chain due diligence and compliance best practices.

All automotive companies would do well to review a January 2019 OFAC settlement with a Californian cosmetics company, e.l.f. Cosmetics, Inc. (ELF), for alleged violations of the North Korean Sanctions Regulations. This settlement occurred after ELF voluntarily reported the “unknowing” importation of 156 shipments of false eyelash kits from two suppliers in China, the contents of which contained materials independently sourced by these suppliers from North Korea. The only “red flags” that the U.S. Government highlighted in support of the penalty were that the U.S. company sourced from China (which was described as a country that frequently deals with North Korea) and that ELF had conducted insufficient due diligence. OFAC, in effect, was treating the lack of supply chain due diligence and compliance measures as equivalent to knowledge of the alleged violations.11

The U.S. Government highlighted “two primary risks” for international sourcing and supply chains: (1) the inadvertent sourcing of goods, services, or technology from North Korea; and (2) the presence of North Korean citizens or nationals in companies’ supply chains, whose labor generates revenue for the North Korean government.” To avoid these alleged violations, the U.S. Government concludes that “[b]usinesses should closely examine their entire supply chain(s) for North Korean laborers and goods, services, or technology, and adopt appropriate due diligence best practices,”12 including what OFAC referred to as “full-spectrum” due diligence on suppliers operating in high-risk environments. The same reasoning would apply equally for other strict economic sanctions, such as those in place against Iran, Russia, Venezuela, or other countries.

For automotive companies, many of which often rely on far-flung supply chains, the warning from the ELF settlement is clear: the U.S. government expects companies to conduct due diligence and apply know-your-supplier compliance measures for all purchases from high-risk regions, like China and Mexico.

A well-run compliance program, however, is not something that comes about by accident – particularly in the international realm. Natural changes in the organization’s footprint, evolving methods of operation, changes in the law (such as the new sanctions on Iran), and shifts in the enforcement aims of government authorities all conspire to make even the best compliance program obsolete in a surprisingly short time. Thus, to stay one-step ahead of the U.S. government’s increasingly aggressive enforcement of export laws and international conduct, any automotive company that has not yet conducted a risk-assessment or recently reviewed the effectiveness of its international compliance efforts should consider doing so – today.

If you would like a sample risk assessment questionnaire, or a guide to compliance best practices for automotive companies, please contact the authors at [email protected] or 202.945.6149, or at [email protected] or 202.295.4001.

What We Know Now – Lessons from 2019 to Better Manage Data Privacy in 2020

By Chanley Howell, Partner, Tom Chisena, Associate, and Chloe Talbert, Law Graduate

Over the last year, technology innovations in the automotive industry continued to be a boon for both drivers and manufacturers alike, particularly in the area of connected cars and autonomous vehicles. However, with big gains in technology come big data, and 2019 delivered the next big wave of data privacy and security laws to regulate that data. This past year alone, we saw many jurisdictions at both the state and national level (including California, Maine, Nevada, New York, Massachusetts, Texas, Kenya, and Thailand) introduce or implement new privacy and security regulations that have or would impact automotive industry consumers and other users of connected cars. This new wave of regulation comes on the heels of the European Union’s General Data Protection Regulation (the GDPR) implemented in May 2018.

But it’s not just new laws and regulations pressuring automotive industries on their data management practices. Consumers themselves are also a driving force of privacy scrutiny both inside and outside of the automotive industry. As automotive technologies become more personal and targeted, the individual becomes more vulnerable, and consumers are now expecting that their vehicle’s data privacy and security protections match the functionality and advances in smart technology. While compliance with data privacy regulations can create new business and operational challenges, noncompliance can result in harsh monetary and legal penalties, including steep fines and potential civil liability. A potentially even greater consequence of noncompliance could be the loss of consumer trust. Just like a cybersecurity breach may signal to consumers that their data is not safe, a company’s breach of applicable data privacy laws could send a similar message. As consumers continue to prioritize privacy, companies that cannot keep up with consumer expectations or regulatory requirements could lose reputation and goodwill in the marketplace. Accordingly, we expect to see in 2020 that a company’s culture, policies, and practices regarding data privacy and the protection of personal information will become an important consideration for consumers in the marketplace. Regulatory compliance likely is the first step to building the kind of culture and reputation around data privacy that companies will need to gain and maintain consumer trust moving forward.

The complexity of the regulations and their varying geographic scope and industry applicability, as well as the business and operational burdens they may impose, make navigating data privacy compliance and security practices difficult. However, we outline below some guideposts that are emerging in this area as your company thinks about how best to comply with regulation as well as secure and maintain consumer trust as data privacy laws and consumer expectations continue to evolve.

Data Privacy and Compliance Issues and Best Practices

We now know that regulators and consumers are aligned with respect to protecting consumers’ personal information, data, and privacy and are looking to hold companies accountable for providing those protections. This shift towards prioritizing privacy is creating new challenges as companies work to strengthen their data privacy and security to comply with regulation and consumer expectations. However, this shift has also created an opportunity for companies to become industry leaders in this area, and knowledge of the current issues and best practices to address them is the first step towards setting that precedent.

1. Navigating and Understanding Applicable Law

The number of new privacy laws and their varying scope makes compliance particularly challenging for companies with diverse or widespread operations, as it can be difficult to establish exactly which regulations apply, depending on companies’ geography or industry, and on how, why, and what kind of data companies are dealing with. Understanding how companies’ operations fit into these privacy schemes is crucial for continued regulatory compliance. Implementing and fostering a strong unified privacy and security program can help companies navigate this web of regulation, and create a strong foundation that can provide consumers the security they demand while still maintaining the flexibility to adapt to the specific needs of a particular jurisdiction or regulation as data privacy compliance requirements expand and evolve. A strong unified privacy effort may also engender trust and security in consumers.

2. Third-Party Risk Management

Third parties can create additional liability for companies and consumers. While companies may implement internal measures to build consumer trust and maintain regulatory compliance, they could risking losing that trust if they engage with a third party that fails to comply with applicable data privacy laws or otherwise puts consumer data at risk. Companies should incorporate data privacy and security review into their due diligence when engaging with vendors or other third parties, especially those that deal with consumers’ personal information. Companies should review third parties’ data privacy and security practices to ensure that they align with their own and are compliant with applicable regulations. In the event that third parties will deal with consumers’ personal information, they should be bound to maintain compliance and meet companies’ standards of privacy and protection, and be held responsible if they fail to do so. Transparency surrounding companies’ use of third parties may additionally bolster consumer trust by mitigating the risk of an unknown and by shifting some of the burden of compliance or customer concern. This could be particularly important for third parties with which companies have ongoing relationships or that deal with particularly sensitive personal information. Companies should disclose relationships with these third parties up-front, and reference their privacy policies or other relevant data privacy and security documentation for consumers to review. Where appropriate, companies should additionally provide relevant contact information for these third parties, so consumers can address any questions they may have regarding privacy policies and practices or voice specific concerns regarding data or personal information in a third party’s possession.

3. Forecasting Operational and Business Requirements

Companies need to be proactive as consumer demand for stronger data privacy and security protections and the regulatory response continues, and should start by analyzing their compliance requirements. In adding additional protections and control for consumers, privacy laws create operational and technological burdens on companies. For example, notice and request for information requirements may require additional employees and training, and companies’ systems and technical practices may need to be updated to implement and support required protections like data anonymization and aggregation. Companies should stay up to date on emerging privacy and security issues, and should continue to prepare their operations for upcoming regulations or protections. Companies should also look beyond the letter of the law, and should forecast their privacy and security practices in response to technological innovations, as they will have the greatest understanding of what risks the technologies may pose to privacy and how best to respond. Companies should maintain an offensive strategy when it comes to privacy, as playing catch-up could result in noncompliance.

4. Consumer Expectations and Securing Consumer Trust

As consumers become more aware of their data and more concerned with privacy, they are demanding greater transparency, protection, and control over personal information. Further, how companies meet these demands is becoming a priority for consumers in the marketplace, and companies that do not earn the trust of consumers with regard to privacy may start to fall behind. Companies should make privacy a priority, and make that priority obvious to consumers. With this shared interest as a foundation, companies should additionally be transparent about their privacy policies and practices and should engage with consumers’ questions or concerns. Cultivating this kind of trust is crucial as connective and autonomous innovations and privacy concerns continue to grow.

5. Remember that Cybersecurity ≠ Compliance

While compliance with data privacy regulation is necessary, it may not always be sufficient to protect data. Third parties may continue to pose cybersecurity risks, as discussed above, and while compliance with notice and opt-out/ opt-in requirements implemented by privacy laws may give consumers more control over and information about authorized uses or disclosures of their data, it does not protect them from unauthorized uses or disclosures. Companies should continue to work to implement security measures and practices that work to provide the best cybersecurity, including eliminating vulnerability early at the design stage and continuously monitoring and preparing for new or inevitable security threats.

Conclusion

Consumers and regulators appear to now agree on the need for stronger data privacy protections, as connectivity and the personalization and automation of technologies continues and as more and more personal information is collected about users. This continues to place added pressures on the automotive industry as a whole. Virtually all facets of the organization, and sometimes third parties as well, will need to be involved to properly plan, implement protections, and prepare for compliance with new and expanding regulations and consumer demands. There is an opportunity to lead the pack in this evolving area, and taking action now will give your company a head start as 2020 arrives.

The USMCA, with the December 2019 updates, will soon take effect. Here’s what to expect.

By Alejandro Gomez, Partner, Marco Najera, Partner and Fernando Camarena, Partner

1. Updated USMCA will pass

While the U.S.-Mexico-Canada Agreement (USMCA) was signed on November 30, 2018, subsequent pressure from U.S. House of Representatives prompted major updates to the agreement and a USMCA’s Protocol of Amendment was signed on December 10, 2019. The amended USMCA is on track to enter into force around mid-2020 — three months after all parties have completed their internal ratification procedures, with exclusively Canada still waiting on Congressional approval.

The USMCA presents some challenges for the automotive industry. Increased percentages in Regional Value Content (RVC) will be required — and the percentages will continue increasing for a number of years — a new Labor Value Content (LVC) element will be compulsory, and auto parts are meticulously divided in several “tables” with varying and increasing percentages to qualify as originating. Additionally, beginning seven years after the amended USMCA enters into force, a passenger vehicle, light truck or heavy truck will be considered as made in the region only if, during the prior year, at least 70% of the vehicle producer´s purchases of steel qualify as originating as well. Regarding aluminum, 10 years after entry into force of the amended agreement, the parties — the U.S., Canada and Mexico — will determine how to consider it as originating.

But despite the RVC and LVC requirements, as well as those pertaining auto parts, being known and unchanged for more than a year, many companies could end up determining, on an expedited basis, how to cope with a complex, multi-tiered, and likely cross-border supply chain.

We also should not lose sight that a company’s compliance or lack thereof with USMCA’s Rules of Origin (ROO) may bring rather different results, from including exemption of import duties on one end, to paying 2.5% for certain automobiles, or 25% for certain vehicles for transportation of goods under World Trade Organization rules to the other.

But there were other important changes stemming from the December 2019 update. In addition to the aforementioned provisions for the 70% requirement on steel and eventually aluminum, Mexico must comply with newly passed labor law provisions. We believe Mexico has successfully shown its commitment to properly enforce changes included both in USMCA and its update, and in resisting tougher U.S. and Canadian oversight within its borders pertaining freedom of association and collective bargaining, though both countries have a facility-specific, rapid-response revision mechanism, which may be revised by a panel of labor experts. The burden of proof is on the defending party to demonstrate that a violation does not affect trade or investment between the parties. Additionally, the position of Mexico-based Labor Attachés was created, which will provide firsthand information regarding Mexico´s labor practices.

Regarding environment concerns, the burden of proof shifts for the defending party to demonstrate that an environmental violation does not affect trade or investment among the parties – just as it does in labor matters. Parties must implement the respective obligations under their multilateral environmental agreements. Also, the position of Environmental Attachés was created to monitor Mexico´s environmental enforcement.

Updated USMCA guarantees regarding state-to-state dispute settlement provisions mean a party may not block the formation of panels and, pertaining to intellectual property, parties agreed to remove the mandatory 10-year data protection for biologics, and to individually maintain their domestic policy priorities.

As to investment-recipient “winning” countries within USMCA, it is not for governments to brag about it beforehand; likely results will be a sum of individual OEM´s model-based decisions and corresponding multiplying effects in production chains. We believe, though, that Mexico will surely receive greater investments regardless of the LVC requirement because the party that adds lower costs to a specific, model calculations will always be considered.

Additionally, non-USMCA located suppliers will move to the country to continue being considered by an already defined inventory of OEMs in Mexico, and the country will benefit from a demographic boon during the next several years that will help neutralize the dwindling U.S. population, and necessarily, its workforce.

We should again remind ourselves that the forthcoming USMCA approval by the three parties will provide much-needed certainty and stability for North America to build upon individual strengths and effectively compete globally as a single trading bloc.

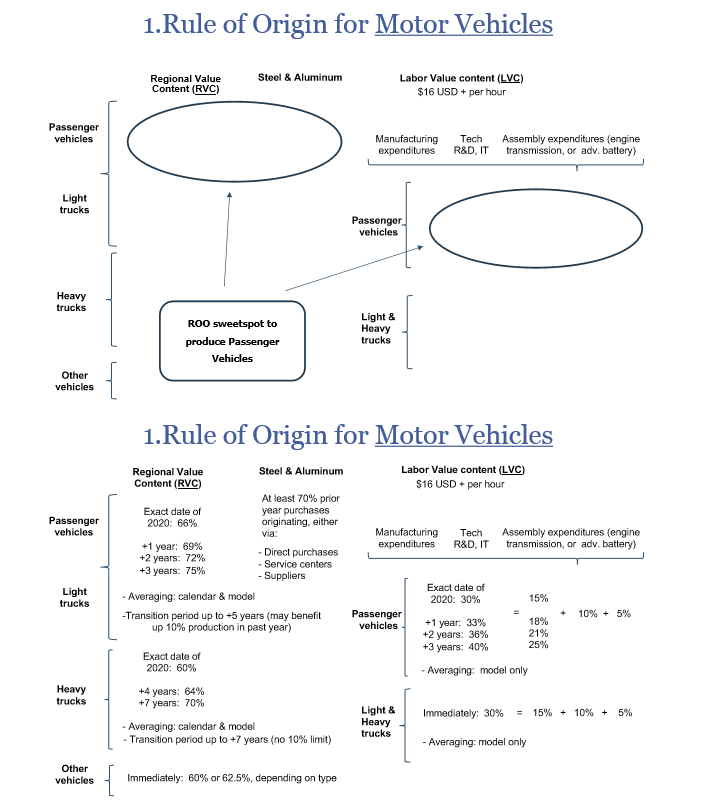

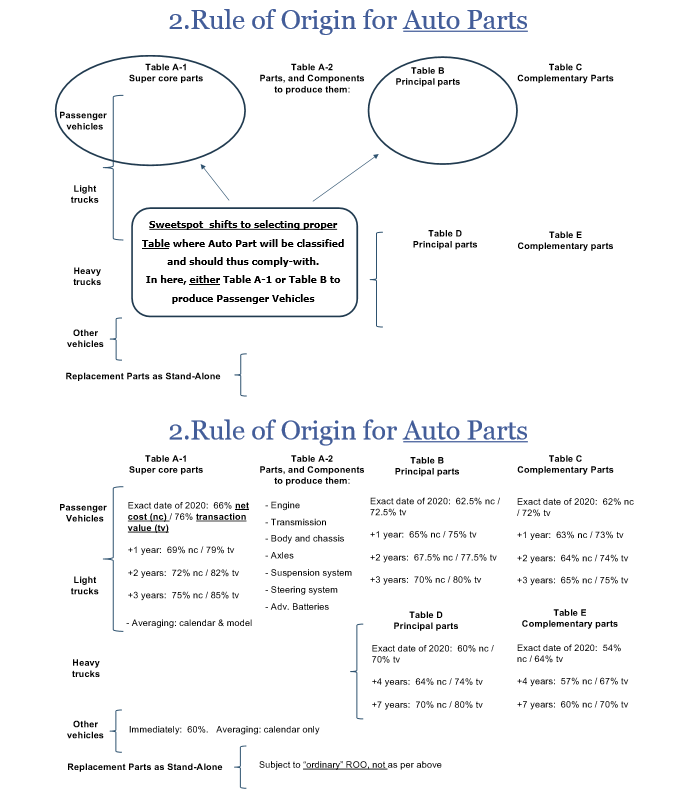

2. Is your company prepared to comply with USMCA’s ROO for motor vehicles and auto parts?

What was unchanged from the original USMCA is certainly relevant to the automotive industry. The following charts are a summary of the rules, percentages and requirements that are going to be enforceable in a few months’ time.

This summary simplifies the amended USMCA’s Chapter 4, Rules of Origin provisions to manufacture motor vehicles and auto parts in North America.

USMCA’s Rules of Origin (ROO)

- Following slides present “Exact date of 2020” USMCA approval as starting point, which triggers +1, +2, +3… year periods.

- Exclusively enforcement of 70% steel requirement postponed for 7 years. Rest of following details, known for +1 year.

- The secret lies in finding your sweetspot in following slides as your company will NOT have to comply with ALL of the incoming relevant rules.

- For full summary of USMCA’s ROO for motor vehicles and auto parts visit: https://www.foley.com/en/insights/ publications/2018/11/understanding-and-coping-with-the-usmexicocanada-a

3. New labor provisions

In anticipation of USMCA’s approval, Mexico recently passed significant legal provisions dealing with labor.13

Possible impacts to employers derived from relevant changes are as follows: as workers become aware of legal modifications, they will likely question the status quo of their unions; “protection” labor contracts (i.e., those signed with unions friendly to employers) will likely face challenges and, on a company-by-company basis, be replaced by other contracts or ratified; depending on unions’ specific offers, workers would decide to stay in them, leave or form / join a new union; many older union leaders will likely be replaced by new ones who seek to address what is or may be bringing restlessness to the workforce; unions may increase demands for economic support – a common practice in Mexico – due to the expansion of their internal workloads; and human capital areas of companies, as well as outside counseling, will need to be strengthened.

4. New 2020 tax law

Even though unrelated to the amended USMCA, a comprehensive 2020 Mexican Tax Reform aimed at increasing collections was passed and, with most of its provisions taking effect January 1, companies doing business in the country need to be aware of relevant changes.14 Approved new rules follow in many cases the recommendations of the OECD´s Base Erosion and Profit Shifting Project Final Report (BEPS).

A very broad General Anti-Avoidance Rule (GAAR) will allow the Mexican Treasury to recharacterize transactions in which lack of business purposes are deemed to exist. Also, new deduction limits in the case of payments to low tax jurisdictions, as well as hybrid structures and interest, were implemented. Changes to the definition of permanent establishment will make Mexican legislation more aligned with OECD rules. Controlled foreign corporation (CFC) rules and the regime applicable to foreign pass-through entities were subject to substantial changes. The shelter Maquiladora regime was also amended to include an indefinite duration, replacing its previous 4-year duration term.

Additionally, the Mexican Income Tax Law and the Value-Added Tax Law were amended to include rules to cover the digital economy. These rules apply to Mexican individuals (tax residents) that sell goods or provide services through digital platforms and to non-Mexican residents (with no permanent establishment) for digital services deemed to be provided in Mexico.

To strengthen outsourcing activities rules, taxpayers who receive such services must withhold a portion of the ValueAdded Tax with respect to the outsourcing payments they make. Criminal Tax reform was also passed so that, in certain cases, the sale and deduction of fake invoices could be deemed as similar to organized crime.

Finally, there are bills in the Mexican Congress that, if approved, would result in more complex rules to further regulate outsourcing activities in Mexico, both from a labor and tax perspective. Companies should monitor these possibly-incoming new rules as they could entail substantive changes in their structures.

5. Anti-corruption and product-safety provisions

Additionally, companies doing business in Mexico should not lose sight of already existing, yet not as-known, obligations. They should be careful in adopting anti-corruption and integrity policies to meet Mexican anti-corruption rules as well as the U.S. Foreign Corrupt Practices Act (FCPA). Sanctions for engaging in corrupt practices in Mexico have severe economic and criminal consequences; for example, companies and individuals can be sanctioned with fines of up to two times the acquired benefits, damages, and lost profits, as well as temporary disqualification from participating in public bids. Implementing anti-corruption and integrity policies conforming with both jurisdictions, as well as continuing anti-corruption training programs to employees, are effective tools to mitigate associated risks.

Entities doing business in Mexico should be also careful in complying with international (e.g., U.S.) and Mexico safety standards to avoid potential risks of damage claims and class actions, as well as penalties and recall procedures that can be imposed by the Mexican consumer protection agency (Profeco).

NHTSA and Motor Vehicle Safety

By Christopher H. Grigorian, Partner, R. Nicholas Englund, Special Counsel

Introduction

The continued development of advanced driver assistance systems (ADAS) and automated vehicles (AV) has rendered many of the assumptions underpinning today’s vehicle safety regulations out of date. The National Highway Traffic Safety Administration (NHTSA) – the primary regulator of motor vehicles and motor vehicle equipment – has thus been racing not only to understand these new technologies, but also to balance its safety mission with the Trump Administration’s goal of removing regulatory barriers on such innovations. Meanwhile, Congress has been working with the automotive industry and other stakeholders to clarify the role of federal and state regulations. Despite the public attention and NHTSA resources showered on these exciting new technologies, the Agency also remains focused on its traditional enforcement work.

Modernizing NHTSA’s Regulations

NHTSA developed most Federal Motor Vehicle Safety Standards (FMVSSs) at a time when the state of technology required each vehicle to have a human driver, necessitating manual controls, displays and telltales, and a clear view of the driving environment. These assumptions do not apply to technologies that automate driving functions and may limit vehicular operation to specific routes or environmental conditions.

To address these new technologies, NHTSA is actively working to modernize the FMVSSs, as well as other regulations – all while reducing regulatory barriers. In the fall of 2019, the U.S. Department of Transportation (U.S. DOT) explained, “NHTSA plans to issue regulatory actions that: (1) allow for permanent updates to current FMVSS reflecting new technology; and (2) allow for updates to NHTSA’s regulations outlining the administrative processes for petitioning the Agency for exemptions, rulemakings, and reconsiderations.”15

Over the past few years, NHTSA has issued a series of advanced notices of proposed rulemaking (ANPRM) that have progressed from general requests for comments on potential regulatory barriers for new technologies, to requests for comments on specific standards. In 2019, NHTSA published ANPRMs seeking comments on:

- The near- and long-term challenges of testing and verifying compliance with existing crash avoidance safety standards (the 100-series FMVSS) for vehicles that lack traditional controls;

- Permitting camera-based rear visibility systems as an alternative to inside and outside rearview mirrors (as currently required by FMVSS 111); and

- Updating tire performance requirements related to the strength test, bead unseating resistance test, and tire endurance test, as well as issues related to new tire technologies.

NHTSA plans to publish additional requests for public comment on modernizing existing regulations and removing regulatory barriers. For example, the Agency has announced plans to issue an ANPRM to update the lighting standards in FMVSS 108, specifically looking at the effectiveness of various design-oriented provisions – such as minimum lamp size requirements, optical material certifications, and headlamp bulb marking requirements – as well as alternatives that would make the standard more performance-based. The ANPRM will also seek comments on updating the lighting standard to address requirements that may no longer be effective or that unnecessarily inhibit the adoption of modern lighting technology. NHTSA also anticipates finalizing previously proposed amendments to the lighting standard to permit adaptive driving beams (ADB) – an amendment initially proposed in late 2018. And NHTSA is considering the applicability and appropriateness of requiring safety messaging through telltales, indicators, and warnings in vehicles without human drivers and conventional driver controls.

In conjunction with its efforts to modernize existing regulations, NHTSA is developing test procedures to assess the performance of certain ADAS technologies that have entered, or will soon enter, the market. In a November 2019 request for comments, NHTSA sought comments on the development of test procedures aimed at objectively and practically assessing the performance of the following systems:

For light vehicles:

- Active parking assist

- Blind spot detection

- Blind spot intervention

- Intersection safety assist

- Opposing traffic safety assist

- Pedestrian automatic emergency braking

- Rear automatic braking

- Traffic jam assist

For heavy vehicles:

- Forward collision warning

- Automatic emergency braking

The development of these test procedures is not part of a current rulemaking. Nonetheless, the tests the Agency develops will likely lay the foundation for potential changes to the New Car Assessment Program (NCAP) and future safety standards related to these technologies. To ensure that these tests reasonably reflect real-world safety and remain technology neutral, manufacturers developing ADAS and AV technologies in such areas should watch these developments closely and share with NHTSA any insights they have learned in developing objective tests for these functions.

In addition to amending safety standards, NHTSA is reviewing its regulations concerning rulemaking petitions. Because the Agency developed the petition process prior to the introduction of technological innovations encompassing multiple regulations, NHTSA is looking at the benefits of streamlining the existing process for the receipt, review, and processing of rulemaking petitions.

NHTSA’s modernization efforts dovetail with its review of recent petitions for temporary exemption from certain safety standards. Current temporary exemption regulations potentially offer a short-term solution to existing regulatory barriers by permitting the Agency to exempt up to 2,500 vehicles when NHTSA determines that the exemption is consistent with public interest and the objectives of the National Traffic and Motor Vehicle Safety Act (Safety Act). We note that NHTSA’s regulations limit such petitions to vehicle manufacturers, leaving no pathway for parties such as suppliers and technology companies to seek an exemption.

At present, there are at least two exemption petitions covering highly automated vehicles pending before the Agency. NHTSA’s resolution of these petitions is likely to provide a clearer picture as to whether vehicle manufacturers have a reasonable pathway under NHTSA’s current exemption authority to deploy AVs while NHTSA continues the process of modernizing existing safety standards.

Federal Policy on Automated Vehicles 4.0

NHTSA is not alone in its efforts to accommodate advanced transportation technologies. In addition to the U.S. DOT, many other federal agencies have been actively reviewing regulations that may affect automation in the transportation sector.

On January 8, 2020, the White House’s National Science and Technology Council – in cooperation with the U.S. DOT – released “Ensuring American Leadership in Automated Vehicle Technologies: Automated Vehicles 4.0” (AV 4.0). AV 4.0 outlines efforts undertaken across 38 federal departments, independent agencies, commissions, and the Executive Offices of the President, while also providing high-level guidance to federal agencies, innovators, and other stakeholders on the U.S. Government’s posture towards AVs. AV 4.0 documents “a sample of U.S. Government investments and resources related to AVs in order to support American leadership in AV and AV-related research and development.”16

The policy outlines ten principles “to protect users and communities, promote efficient markets, and facilitate coordinated efforts.” These principles include:

- Prioritize safety by facilitating the safe integration of AV technologies, and by enforcing existing laws to prevent entities from making deceptive claims or misleading the public about the performance capabilities of these technologies.

- Emphasize security and cybersecurity by working with developers, manufacturers, integrators, and service providers of AVs and related services “to ensure the successful prevention, mitigation, and investigation of crimes and security . . . while safeguarding privacy, civil rights, and civil liberties” through the promotion of voluntary standards and best practices.

- Ensure privacy and data security using a holistic, risk-based approach that protects drivers, passengers, and passive third parties (such as pedestrians) from unauthorized access, collection, use, or sharing of sensitive data.

- Enhance mobility and accessibility by protecting the ability of consumers to make the mobility choices that best meet their needs, and by treating AV technologies as additional options for consumers to access goods and services.

- Remain technology neutral by adopting and promoting – on an international level – policies that will allow the public, rather than the federal government or foreign governments, to choose the most economically efficient and effective transportation solutions.

- Protect American innovation and creativity through protection and enforcement of intellectual property rights, technical data, and sensitive proprietary communications, and by preventing other nations from gaining any unfair advantage at the expense of American innovators.

- Modernize or eliminate outdated regulations that unnecessarily impede the development of AV and ADAS technologies, and promote a consistent regulatory and operation environment.

- Promote consistent standards and policies by advocating abroad for voluntary consensus standards and by instituting evidence-based and data-driven regulations in collaboration with state, local, tribal, and territorial authorities, as well as industry and international partners.

- Ensure a consistent federal approach through coordinated research, regulations, and policies across the federal government.

- Improve transportation system-level effects by focusing on “opportunities to improve transportation system-level performance, efficiency, and effectiveness while avoiding negative transportation system-level effects from AV technologies.”

The principles described in AV 4.0 largely focus on aspirations for future regulations and describe the work currently underway. Of particular interest to the automotive industry are NHTSA’s research into alternative metrics and safety assessment models, which include assessing a system’s performance and behavior relative to its stated operational design domain (ODD) and Object Event Detection and Response (OEDR) capabilities; the functional safety of a system and related human-factor issues; and occupant protection in alternative vehicle designs. Manufacturers should watch these developments closely, comment on research and proposed regulations, and share their insights with NHTSA.

For the commercial vehicle market, the Federal Motor Carrier Safety Administration (FMCSA) – which regulates the operation of commercial vehicles in interstate commerce – is researching human factors to understand driver readiness, the human-machine interface, adaptation to advanced technologies, and communication with outside vehicles. FMCSA is also researching safety performance of critical sensors, brakes, and tires used in AV technologies, as well as truck platooning, emergency response, and roadside inspections. Manufacturers developing technologies for commercial vehicles should continue following changes at FMCSA and exemptions granted for new technologies, such as recent exemptions for camera monitor systems designed to replace side rear-view mirrors.

Automated Vehicle Legislation

In 2017, the House of Representatives passed the Safely Ensuring Lives Future Deployment and Research In Vehicle Evolution (“SELF DRIVE”) Act, H.R. 3388.17 The SELF DRIVE Act was the first major federal legislative effort to regulate automated vehicles beyond voluntary guidelines. A similar bill, the American Vision for Safer Transportation through Advancement of Revolutionary Technologies (“AV START”) Act, S. 1885,18 moved out of the Senate Committee on Commerce, Science and Transportation by unanimous vote. Despite bipartisan support, the AV START Act never made it to a vote in the Senate, and both the Senate and House bills expired at the end of the last Congress.

In 2019, staff from the Senate Commerce Committee and the House Energy and Commerce Committee have led a bipartisan, bicameral effort to draft new AV legislation. Staff for the respective committees have worked with stakeholders in the automotive industry, public interest groups, states, and federal agencies to understand the need to clarify the roles of state and federal regulations and to remove statutory barriers to advancing ADAS and AV technology. Key points of interest for the automotive industry have been clarifying the preemptive effects of NHTSA regulations on the design and manufacture of motor vehicles and preserving state authority to regulate the licensing and operation of vehicles. The Committees have also been considering granting NHTSA additional authority to exempt AVs from current safety standards. Passing legislation in this area could be of tremendous benefit to the automotive industry by preempting the patchwork of state regulations that may affect vehicle design and providing additional pathways for testing and deploying AVs.

NHTSA Enforcement Actions

While the potential challenges of future technologies pose exciting questions for the automotive industry, NHTSA’s enforcement authority should remain a primary focus for manufacturers’ safety teams. At the close of 2019, the Agency had 44 open defect investigations (18 Engineering Analyses and 26 Preliminary Evaluations) along with ten investigations into the adequacy of manufacturer recalls.19 As these numbers suggest, NHTSA’s investigation efforts remain active and robust.

With respect to penalties, NHTSA recently announced two significant civil penalty agreements that involved late regulatory filings. Unlike many prior settlements, these agreements were not designated as consent orders, but did include provisions similar to consent orders – such as holding a portion of the penalty in abeyance as long as the manufacturers meet certain performance obligations.

Of particular interest, NHTSA and a manufacturer agreed to a $20 million civil penalty based on the Agency’s allegations that the manufacturer repeatedly missed reporting deadlines for various recall reports and related submissions. The violations included failing to timely report a noncompliance to NHTSA, failing to send customer notification letters within the 60-day deadline, and failing to timely submit quarterly recall completion reports.

NHTSA has publicly stated that it continues to monitor compliance with these reporting requirements and will penalize manufacturers that submit documents late or do not timely amend Part 573 reports to include all required information. Notably, NHTSA included seemingly minor violations in the settlement agreement, such as mailing out owner letters 5 or 6 days late and failing to update the remedy schedule to reflect the correct notification date. When a seemingly trivial deadline is missed, manufacturers may believe that NHTSA will not take any enforcement action. Missing deadlines in several recall files, however, could trigger an audit by NHTSA and subsequent penalties. The Agency has the authority to add up all violations – regardless of how minor – in order to increase the penalty amount.

Trends In Leveraging Automotive Patent Portfolios

By Chethan K. Srinivasa, Senior Counsel

In 2019, the automotive industry continued to undergo disruption from various factors, including the movement toward shared economics, electrification, and autonomous vehicles (“AVs”). At the same time, the automotive industry as a whole appears to have experienced stagnant or declining growth.

Under these conditions, automotive companies leveraged large patent portfolios and asserted individual patents. However, they did so in different ways. The following outlines some emerging trends in this space, as well as IP-related challenges the industry will face in coming years.

1. Non-Traditional Leveraging of Large Patent Portfolios by Automakers

Generally speaking, automakers are keen to avoid patent wars20 as they computerize their vehicles – in part, perhaps, because there is insufficient market adoption of electric and/ or AVs to warrant them. Instead of asserting patents, then, some companies with large electric and/or AV patent portfolios may use these patents to tempt rivals into entering the market – thereby indirectly increasing demand for their products.

In 2014, for instance, Tesla pledged21 that they would “not initiate patent lawsuits against anyone who, in good faith, wants to use our technology.” While seemingly altruistic at the time, this pledge was considered by some to be an attempt at promoting electric vehicle technology22 ahead of other early stage technologies (such as hydrogen fuel cells). In 2019, Toyota announced royalty-free access to its nearly 24,000 patents23 designed for vehicles (hybrid and not) using electrification technology. By encouraging adoption of their technology and becoming a supplier for their rivals, Toyota can increase its bottom line by increasing supply and reducing costs associated with24 developing electric vehicles.

Though automakers hope to avoid patent wars when possible, they have by no means abandoned leveraging their patent portfolios to reach their business goals. When the stakes get high enough – which could be within a decade, based on forecasts that predict a $500 billion market for electric vehicles25 and a $60 billion market for AVs26 – automakers may begin asserting their patent portfolios.

2. High-Tech Entrants Asserting Patents

On the other hand, high-tech companies developing innovative connected or AV technologies may not be as hesitant to assert their patent portfolios.

In fact, automobile-related patent litigation by such companies is on the rise27. In 2019, for instance, self-driving car startup Voyage was sued by Sucxess28 for technology related to retrofitting cars with drive-by-wire kits. Sucxess, an “engineering-services firm” – whose founder was formerly an engineer at a traditional automaker – claims that Voyage “wouldn’t exist without these cars … and [they] are getting some real value by using [Sucxess’s] patent.” Taking a page from the high-tech playbook, Sucxess is trying to “make money with [their] own patents.” In another example from last year, American GNC Corp., a technology company that specializes in guidance, navigation, control, and communications, sued Toyota over three AV navigation patents29.

China has also witnessed a large number of high profile entrants30 in the connected, electric, and AV space. Chinese companies typically leverage their patent portfolios to generate licensing-based revenue streams. However, if negotiations around royalty rates for licensing vehicle-related wireless technologies fall through, strategies may shift.

As the number of new high-tech entrants continues to rise, so too may patent infringement suits – as these tech companies port their patent monetization strategies to the automotive space.

3. Challenges in Patenting Autonomous Vehicle AI Technology

While patent portfolios were leveraged in various ways in 2019, it may be challenging to continue developing portfolios in the automotive space, particularly as AV technology increasingly relies on artificial intelligence (“AI”) and software functionality. There are countless hardware innovations being made for AV components, including those for advanced sensors, radar and LiDAR, geolocation, and telecommunications; in 2018, the industry filed 25k+ patents to protect them31. However, as these innovations come to rely more and more on AI and software, the question remains: is it still possible to obtain patent assets for new functionalities or improvements provided by such technologies?

According to the United States Supreme Court, not all innovations are eligible for patent protection. In 2014, the Court said inventions that are directed by abstract ideas or mathematical algorithms may not be eligible to receive patent protection. (Supreme Court case Alice Corp. v. CLS Bank International, 573 U.S. 208 (“Alice”).) Congress also chimed in, holding three hearings in June 2019 on a bipartisan bill that will impact what is eligible for patent protection.

Since these changes make it challenging to obtain patent protection for certain software inventions related to AI or internet of vehicles (“IoV”) technologies, companies may be discouraged from pursuing such protection: since Alice, the number of patent applications filed annually for AI inventions in Digital Marketing, FinTech, Education, and Entertainment actually declined significantly (Industry-Focused Patenting Trends32, page 16).

With Congress yet to finalize the patent reform bill – and since the patent eligibility framework established by Alice left much uncertainty – opinions issued by the U.S. Court of Appeals for the Federal Circuit (“CAFC”) can provide a roadmap for patent eligibility. For example, the CAFC stated that “[s]oftware can make non-abstract improvements to computer technology just as hardware improvements can.” (Enfish, LLC v. Microsoft Corp., 822 F.3d 1327 (Fed. Cir. 2016.) The CAFC further emphasized in MCRO, Inc. v. Bandai Namco Games America, decided September 13, 2016, that inventions may be eligible for patenting when “it is the incorporation of … claimed rules, not the use of the computer, that improve[] the existing technological process by allowing the automation of further tasks.” In 2019, the U.S. Patent and Trademark Office provided new guidance33, stating that a claim directed to a practical application of a judicial exception, such as providing an improvement to the functioning of a computer or another technology, is eligible for patent protection.

Most vehicular AI or IoV inventions likely provide such an improvement and therefore may be eligible for patent protection. While we await further clarity from Congress, however, companies should continue building valuable IP assets – as they did for vehicular hardware and manufacturing – by using recent case law to formulate new strategies for protecting AI and software-based AV inventions. The recent attempts at leveraging patent portfolios may be based on hardware or telecommunications patents, but the future patent wars may hinge on those designed for AV software functionality.

2020 Outlook for Automotive M&A: Will the Good Times Keep Rolling?

By Steve Hilfinger, Partner and Igli Psari, Associate

Overview of 2019 and Outlook for 2020

Following a robust and bullish 2018, 2019 saw a modest slowdown in automotive M&A activity and a decline in deal value, due in large part to political and regulatory uncertainty, tariff and trade war impacts, slower global economic growth, and moderating automotive volumes. Most significantly, 2019 saw a major decrease in reported average automotive deal value for larger transactions, with a 50% drop from $235.1 million to $160.9 million year over year. Although these numbers are not final, they appear to signal an overall drop in deal value for 2019. Still, while average deal value may have significantly decreased in 2019, deal volume did not see as steep of a drop, declining by only 3%.